Digital Transformation in Private Banking: How Lombard Lending Is Evolving in Singapore

The private banking sector in Singapore is experiencing a fundamental shift in how lombard loans are originated, managed, and monitored. As wealth management institutions face increasing pressure to deliver faster credit decisions whilst maintaining robust risk controls, lombard lending platforms have emerged as critical infrastructure. Digital lombard loan software now enables private banks to automate complex collateral valuations, streamline approval workflows, and ensure continuous compliance with MAS credit risk requirements.

The Rise of Lombard Loan Automation in APAC Private Banking

Traditional lombard lending processes in Singapore and across APAC markets have historically relied on manual collateral assessments and paper-based approval chains. This approach creates operational bottlenecks that frustrate high-net-worth clients expecting immediate liquidity against their investment portfolios. Modern lombard loan origination systems address these challenges through intelligent automation.

A comprehensive lombard lending platform integrates real-time portfolio data, automated margin calculations, and dynamic risk scoring. Private banks can now process lombard loan applications in hours rather than days. The technology connects directly to custody systems, pulling current valuations and applying predefined lending ratios based on asset class, concentration limits, and client risk profiles.

Wealth lending in Singapore has grown substantially as ultra-high-net-worth individuals seek tax-efficient liquidity solutions. Digital lombard credit automation ensures that private banks can scale their lending books without proportionally increasing operational headcount. The software handles routine tasks such as daily collateral monitoring, margin call generation, and covenant tracking.

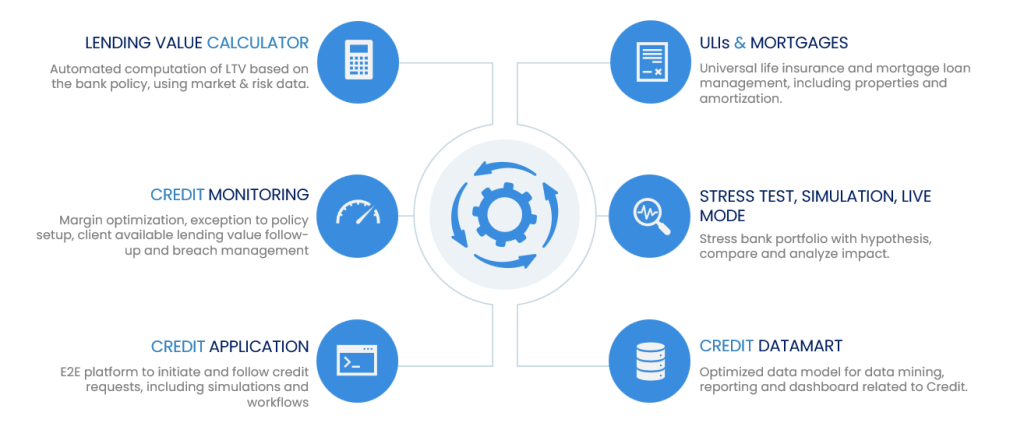

Key Features of Modern Lombard Loan Management Software

Effective lombard loan software must address the entire credit lifecycle. The origination phase requires seamless client onboarding, credit application capture, and preliminary risk assessment. Advanced platforms incorporate digital signature capabilities and automated document collection to eliminate physical paperwork.

The credit decisioning engine forms the core of any robust lombard lending workflow automation system. It applies bank-specific credit policies, calculates advance rates based on collateral composition, and flags concentration risks. Senior credit officers receive structured decision packs with all relevant data points, enabling faster approvals whilst maintaining governance standards.

Post-disbursement, lombard credit monitoring software provides continuous oversight. Daily portfolio revaluations trigger alerts when loan-to-value ratios breach predefined thresholds. Private banking risk software must also track corporate actions, dividend payments, and other events affecting collateral quality. Automated reporting ensures that relationship managers and risk teams maintain full visibility across the lombard book.

Regulatory Compliance and MAS Credit Risk Standards

Singapore’s regulatory environment demands rigorous credit risk management frameworks. MAS credit risk compliance requirements specify clear standards for collateral valuation methodologies, stress testing protocols, and concentration limit monitoring. Lombard lending automation platforms embed these regulatory requirements directly into system workflows.

Digital solutions maintain comprehensive audit trails documenting every credit decision, collateral adjustment, and policy override. This transparency proves essential during regulatory examinations. The software also facilitates stress testing by modelling portfolio performance under various market scenarios, helping private banks quantify potential losses and maintain adequate capital buffers.

Wealth management technology in Singapore increasingly incorporates artificial intelligence for enhanced risk detection. Machine learning algorithms identify unusual patterns in client behaviour or collateral movements that might indicate emerging credit concerns. This proactive approach aligns with regulatory expectations for sound risk management practices.

Regional Considerations for APAC Wealth Lending

Private banking lombard loans across APAC markets present unique challenges compared to Western jurisdictions. Multi-currency lending is standard, requiring sophisticated foreign exchange risk management. Collateral pools often include assets held across multiple custodians in different countries, demanding robust data aggregation capabilities.

Hong Kong, Singapore, Malaysia, Thailand, Indonesia, and the Philippines each maintain distinct regulatory frameworks governing secured lending. A scalable lombard credit monitoring platform must accommodate varying margin requirements, documentation standards, and reporting obligations. Leading private banks deploy unified technology platforms that can be configured for local market requirements whilst maintaining consistent global risk standards.

Cultural factors also influence lombard lending practices in APAC. Relationship-driven banking models require technology that enhances rather than replaces human interaction. The best lombard loan management software provides relationship managers with instant access to client credit positions, enabling informed conversations about additional borrowing capacity or portfolio optimisation strategies.

Selecting the Right Lombard Lending Platform

Private banks evaluating lombard loan software should prioritise several critical capabilities. Integration with existing core banking and portfolio management systems is essential to avoid data silos. The platform must support complex collateral structures including listed securities, bonds, funds, and alternative investments.

Scalability matters as lending volumes grow. Cloud-based lombard lending workflow automation solutions offer flexibility and reduced infrastructure costs. Security and data protection remain paramount given the sensitive nature of client financial information.

Vendor expertise in private banking credit processes distinguishes truly effective solutions from generic lending platforms. Purpose-built lombard credit automation systems incorporate industry best practices developed through years of implementation experience across leading wealth management institutions.

For private banks seeking to modernise their credit operations, exploring specialised solutions designed for APAC markets provides a strategic advantage. SpeciTec’s Credit & Risk Monitoring platform offers comprehensive credit lifecycle management capabilities tailored to regional requirements.

The Future of Lombard Lending in Singapore

Digital transformation in lombard lending continues to accelerate. Emerging technologies such as blockchain-based collateral registries and real-time settlement systems promise further efficiency gains. Private banks that invest in robust lombard loan origination systems today position themselves to capitalise on growing wealth lending opportunities across APAC.

The competitive landscape increasingly favours institutions that can deliver superior client experiences through technology. Fast credit decisions, transparent pricing, and proactive portfolio monitoring differentiate leading private banks. Lombard lending automation is no longer optional but essential infrastructure for wealth management success.

Singapore’s position as a premier wealth management hub depends partly on the sophistication of its financial infrastructure. As reported by the Monetary Authority of Singapore, continued investment in financial technology strengthens the jurisdiction’s competitive position. Private banks embracing digital lombard credit monitoring software contribute to this broader ecosystem development.

Ready to transform your private banking credit operations?

Discover how SpeciCRED delivers comprehensive lombard lending automation designed specifically for APAC private banks.

Frequently Asked Questions About Lombard Lending

What is a lombard loan in Singapore?

A lombard loan is a secured credit facility where clients borrow against their investment portfolios. Private banks in Singapore offer lombard lending to high-net-worth individuals seeking liquidity without liquidating assets.

How does lombard loan software improve credit processing?

Lombard loan management software automates collateral valuation, margin calculations, and approval workflows. This reduces processing time from days to hours whilst maintaining robust risk controls and MAS compliance.

What collateral types can be used for lombard loans?

Typical collateral includes listed equities, bonds, mutual funds, and structured products. Advanced lombard lending platforms support complex multi-asset portfolios with automated concentration limit monitoring.

How do private banks monitor lombard credit risk?

Lombard credit monitoring software provides daily portfolio revaluations, automated margin call generation, and real-time breach alerts. This ensures continuous oversight of loan-to-value ratios and collateral quality.

Why is lombard lending automation important for APAC private banks?

APAC wealth lending involves multi-currency exposures, cross-border collateral, and diverse regulatory requirements. Automation ensures scalability, consistency, and compliance across different jurisdictions.

Alberic Vaillant de Guelis

Singapore Director at SpeciTec. Focuses on Lombard credit, risk monitoring and the digital transformation of private banking in APAC, with a strong emphasis on scalable credit platforms and operational efficiency.